I picked up some shares in Macau E&M Holding (1408.HK) recently. The terrible sentiment for Hong Kong listed stocks for the last few years is well known. Macau E&M shows nicely how far share prices can fall in an environment like this. I think there are some positives to be found at this company though and believe it is a good candidate for a diversified basket of net-nets.

I usually size positions like this at 1%-2%. If I can find a bunch of them when they are out there, they can help round out my portfolio. I think it is generally a terrible idea to concentrate in a company like this. There are just too many nasty surprises out there in Hong Kong micro-caps. It really is a minefield.

Some financial data for the company:

Share price: $0.14

Outstanding shares: 500.0m

Market cap: $70m HKD -> 72.1m Macau Pataca (MOP)

Net loss 2023: (3.8m MOP)

Net cash: 129m MOP. Cash and deposits: ~142m. Debt: 12.8m MOP.

The first thing that jumps out is that Macau E&M is a very small company. The market cap is currently $72.1m Macau Pataca (MOP), or around $9m USD. The free float is much smaller than that because the company’s insiders own 75% of the outstanding shares. So the free float is probably only around $2.3m USD. This company is really among the smallest of Hong Kong listed companies. Usually these very small companies have terrible issues. I think Macau E&M looks a lot better than most in that group though.

General

Macau E&M is an electrical and mechanical (“E&M”) engineering services works contractor in Macau. They provide HVAC system works and low voltage system works for the public sector and the private sector. Their private sector customers are primarily hotels and entertainment resorts. Demand from this group is tied to the performance of the casino’s in Macau.

The casino’s in Macau have had a tough time during Covid and the environment is still depressed. Things do seem to be improving with the reopening of the borders with Mainland China, but the E&M sector has continued to lag.

There was also uncertainty around the granting of new casino licenses. These were finally granted at the end of 2022 for a period of 10 years and came into effect on January 1, 2023. It seems likely that casino’s have held back certain projects until their licenses were extended. It is interesting that 90% of the investment by the casino’s will go to non-gaming projects. Hopefully Macau E&M will be able to get a piece of that pie, but this didn’t happen yet in 2023.

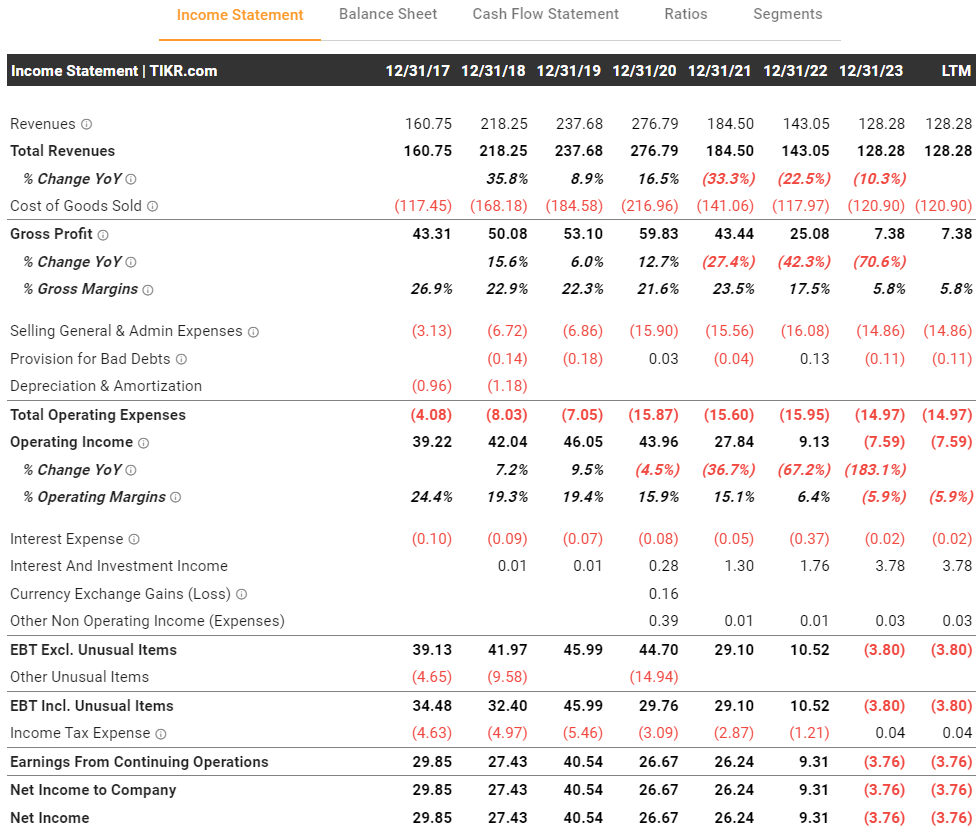

Recent and historical results

Macau E&M lost 3.8m MOP in 2023, so a very small loss. It is encouraging that the company has already showed some signs of improvement: in H1 Macau E&M had a loss of $5.4m MOP, but the loss for the full year was only $3.8m MOP, so the second half was (barely) profitable.

In prior years the performance was a lot better:

Source financials: TIKR.com

Profits have been north of 25m MOP before the Covid years. I think that shows the potential earnings power of the company in a somewhat normalized environment. The problem is that I can’t tell when a reasonably good year will come again. But I don’t think that is really necessary at the current price. I think that within a couple of years we could see the company earning 15-20m MOP again. And if that happens, the company will probably look awfully cheap to more investors.

Potential for a very large dividend

What makes this company particularly interesting to me is the potential for a very large dividend payment when the company returns to solid profitability. The reason why I think that could happen is that they have done it before in 2021 (dividend paid out during 2022):

Subsequent to the end of the Year, the Board has recommended the Final Dividend of HK2.03 cents (2020: Nil) per Share for the year ended 31 December 2021 to the Shareholders.

In light of the retained earnings of the Group as at 31 December 2021, without prejudice to the healthy and sustained development of the Company, in order to offer a better return for the Shareholders, the Board has recommended the Special Dividend of HK3.97 cents per Share for the year ended 31 December 2021 to the Shareholders in addition to the Final Dividend.

Source: page 74, AR 2021. Bold text mine.

So after a year in which the company had earnings of $26m and a cash balance of $174m, they paid out ~$31m in dividends (0.06 HKD per share). Compared to the current market cap of 72m, that would be a huge number. It is probably a bit too optimistic to assume that earnings will recover quickly and the company will decide to pay out a similar amount, but I think the 2021 dividends are a very positive sign. The company has shown it is willing to pay out a very large dividend when earnings are solidly positive and when there’s a big cash balance. The big cash balance was already there at the end of 2023, but the earnings aren’t there yet.

Instead the company decided not to pay a dividend at all in 2023. This has probably contributed to the fall of the share price. There are plenty of companies in Hong Kong offering juicy dividends, so why stick with some unprofitable, illiquid micro-cap that has just cut the dividend? I disagree with that view though, because management has shown that it is willing to pay a very large dividend if it is supported by current earnings.

Of course, the company could have decided to pay a dividend for 2023 even though the company had a small loss. Why they didn’t, I don’t know. I think this could be because they don’t want to look bad and pay out a lot of cash when the Macau economy isn’t doing well and a lot of businesses and people are having a tough year. The fact that management did not pay a dividend does not make them shareholder unfriendly, or unwilling to pay a large dividend in the future. I think the fact that they did pay a very large one in 2021 should weigh a lot heavier than the fact that they decided not to pay a dividend in 2023. It seems the market doesn’t see it that way.

I wouldn’t be surprised to see 20-30% of the current market cap paid out as a (special) dividend when operations recover. That should be the main catalyst for the stock.

Outlook

What I like about the management in the annual report is that they do go into a bit of detail about the performance of the business. Many Hong Kong listed companies hardly discuss the drivers over their performance at all, which leaves investors largely in the dark about the reasons for the performance of the business. For example, Macau E&M explained that a reason for the losses in 2023 was their decision not to fire employees in 2023 but to keep them in the workforce to be positioned well for any recovery:

The main pressure for the Group was from salary expenses. With no staff redundancies during the Year, it had to bear the burden of heavy staff costs, and the very narrow project margins were insufficient to cover both fixed costs and salaries.

Source: page 9, AR 2023

[…] due to the above factors, the revenue from certain projects with low profit margin was not able to cover all the associated fixed costs and salaries of the Group. However, the Group still strives to be socially responsible and with a view to maintain its competitiveness and capability, the Group has maintained its existing workforce without any staff redundancies during the Year.

Source: page 11, AR 2023

This means that 2023’s financial performance was probably a bit worse than it had to be. Still, this makes sense to me because it can be hard to find and quickly bring on the right people again when operations do turn around.

Management sounds optimistic about a significant rebound of operations in 2024:

The reopening of the borders with Mainland China and the renewed casino licenses have given the market a much-needed boost. That optimism, however, has not yet turned into business transactions either. Both the government and private sectors have remained prudent in embarking on project initiatives. The Group expects to see a significant belated rebound in around mid to late 2024. With a solid foundation and in a stable financial position, the Group is well-poised to welcome a thorough economic recovery and it is on its way to recover the business in general. This is why the Group in general

remains cautiously optimistic about the market and the E&M industry in Macau.

Source: page 14, AR 2023. Bold text mine.

Conclusion

Hong Kong companies are always somewhat of a black box to me. With a micro-cap like this, it is no different. Sometimes I find something that looks very attractive, but then management does something crazy. A nice recent example is G&M Holdings (6038.HK). This looked like a nice cash-rich micro-cap in the construction sector with a history of solid dividend payments. Then in June 2023, they suddenly decided to invest a substantial amount of cash in a coal mine. That is a situation I want to stay away from.

I haven’t seen this sort of thing at Macau E&M yet. They did make a large investment of 33.0m HKD in property during 2022, but this property is used as their new head office and replaced their leased offices. I think that is OK. Still, Macau E&M is a relatively recent IPO (2020) so the risk of bad capital allocation or any shady behavior is bigger than at companies with a longer track record as a public company.

For an investment to work out well here, much will depend on the timing of a recovery and if management is willing to pay out a large dividend, as they have done in the past. As part of a basket, I think this company is a good bet at the current price.

Disclosure: long Macau E&M Holding Limited (1408.HK)

Disclaimer: This website is an investment journal of an individual, non-professional investor. It should be read as such.

None of the information presented on this website should be viewed as, or is intended to be, investment advice or a recommendation to buy or sell stock or any other security.

Thanks for the interesting idea! I’m curious just how do you buy stocks with such illiquidity? Just limit order with a pre-determined price?

It can be very difficult to buy a meaningful position sometimes. I tend to watch the ask prices and volumes carefully. If the bid-ask spread is somewhat narrow, I’m not afraid to push the price up a couple of percent if it allows me to get the position size I want.

In illiquid situations, I want my upside to be quite large, so paying a couple of percent more in a completely bombed out stock (many of those around in HK!) shouldn’t affect the outcome of the investment in a few years time too much.

I like to track a lot of different stocks and to keep searching for new ideas, so there’s usually a couple of stocks that are trading around interesting levels and where some volume suddenly appears.

Thanks for sharing with such details. I will try your methods:)

Hi Paul,

Considering the large insider control and cash level, what do you think about the chance of taking the company private? I guess it’s not unlikely because they just IPOed in 2020? Thanks!

There seems to be some speculative action in Macau E&M in the last week or so. Shares have shot up to $0.395 currently. This was on heavy volume as well. The company did release a positive profit alert today, but the expected profit is still very modest as the company continues to muddle along in a period of low construction activity in Macau.

I no longer hold a position in Macau E&M. Even though I missed the last surge in the share price, I’m still happy with the result. It is fair to say though that the company’s results weren’t the catalyst for the increase of the share price. Sometimes these low float stocks just get bid up by a bunch of traders.

Unfortunately many brokers have now blocked trading in these illiquid stocks in Hong Kong. A specialized regional broker is needed to gain access to those stocks again. I have not done that yet, but I perhaps I will open an account in the future.