One sector I like right now is community banks. I own a basket of small, OTC-listed community banks. Last year was a very turbulent year for the banking sector obviously, and even though things recovered quite quickly in the last couple of months, I think there are still a lot of interesting situations to be found among OTC-traded banks.

One such bank is CMUV Bancorp (OTC:CMUV). I think the valuation is modest, but that is true for a great number of banks. I mainly like CMUV for its buyout potential. So I see CMUV more as a special situation investment with a medium time horizon, perhaps around 3 years or so. I don’t expect there to be an immediate catalyst.

Another thing that is notable about CMUV is the capital allocation of the management team. They have made a few significant and timely decisions and, as a result, I think CMUV’s management has greatly increased shareholder value. I’ll describe those decisions below, together with my reasons for believing that the bank is a strong buyout candidate.

Some financial data for CMUV Bancorp:

Share price: $17.08

Shares outstanding (2023-12-31): 1,772,422

Market cap: $30.3m

Total assets Community Valley Bank (subsidiary bank – 2023-12-31 and 2022-12-31): $297.0m , $277.6m

Total securities Community Valley Bank (subsidiary bank – 2023-12-31 and 2022-12-31): $6.2m , $6.2m

Book value CMUV Bancorp 2023-12-31: $28.6m -> $16.15 per share

Minimal securities holdings

One thing that is really striking at CMUV is that there are minimal holdings of investment securities. For the last two years only ~$6m was held in held-to-maturity investments and available-for-sale securities were almost zero. The same picture exists for 2021 and 2020. CMUV held a meaningful cash balance of $45.2m at the end of 2023.

The company was able to avoid the liquidity issues that some other banks experienced because there never was any worry about the value of their securities portfolio due to their immateriality. There wasn’t any reason for depositors to have doubts. CMUV is operating in California and IIRC this state was in the epicenter of last year’s banking panic. CMUV came through without issues and was even able to grow their deposits.

You have to give the bank’s management credit for not reaching for yield in the low interest yield environment that existed and becoming stuck with a large securities portfolio.

Issuing debt at 3.63% to fund a big tender offer

The other management action that I want to highlight is the company’s massive tender offer in October 2021. The company repurchased 20.1% of the outstanding shares at a price of $13.05 per share. They financed this by issuing $7.5m in subordinated debt:

Principal is due on October 26, 2031, and the debt is not redeemable for the first five years except in the event of certain unusual events. Interest only is payable prior to the due date. The interest rate is fixed for the first five years at 3.625% and thereafter floats based on the 90-Day Average SOFR + 2.63%.

Bold text mine

Talk about a timely debt issuance! They locked in the 3.625% rate for this debt for five years and they did this just before interest rates really started to rise. The company can prepay the principal after the fifth year according to the 2021 tender offer document. They then used the proceeds to fund the large tender offer to repurchase 20% of their shares. A tender offer of this size is very rare for a small community bank. To fund it in this way, and at that moment in time, makes it all the more impressive.

So once again, a big compliment should be made to CMUV’s management for nailing the timing of this debt issuance and this tender. I think this created a lot of value for the remaining shareholders.

I think this tender offer in 2021 was the first major step towards a future sale of the company. There are multiple indications that IMO point towards this outcome. I’ll discuss those now.

1. Management’s participation in the tender offers

Besides the big tender offer in 2021, the company completed another tender offer in August 2023. That last tender offer was for 10% of the outstanding shares at a price of $14.25 per share. There was not a lot of interest from shareholders this time: just 45k shares of a potential ~188k shares were repurchased, or about 25% of the maximum number.

I think this is interesting because this second tender was launched after the banking panic hit in March 2023 and still there was not that much interest, even though the price was noticeably higher ($14.25) than in 2021 ($13.05). Of course this ignores the book value of the shares, but still you might expect more people to sell during the events of 2023.

CMUV’s officers and directors participated in the 2021 offer:

Source: CMUV’s 2021 tender offer document

It should be noted that because management only tendered a relatively small number of shares, their overall percentage ownership increased from ~22.7% to ~25.6% of the outstanding shares after completion of the first tender offer.

In the August 2023 tender offer management decided not to participate:

Source: CMUV’s 2023 tender offer document

Why not this time? Who knows, but it could be because insiders know a sale of the company has now come closer and they know they will probably be able to get a much higher price for their shares at that time.

As a side note, what was also unusual at these two tender offers was that there was a very large odd-lot provision of less than 1,000 shares. This meant that any beneficial holder of less than 1,000 shares was not subject to pro-ration and thus guaranteed to get all their shares accepted in the offer. Virtually all tenders have this odd-lot limit set at less than 100 shares. Why did CMUV set this limit at 1,000? Perhaps it was another little push to get small shareholders to tender all their shares by guaranteeing that pro-ration would not be an issue for them.

2. The company leaves open the possibility of a sale

Many small community banks make it no secret that they are proud to be small and independent and that they are looking to keep it that way for many years to come. The son of the CEO is already working at the bank and on the Board of Directors. That sort of thing. This doesn’t seem to be the case at CMUV. Both tender offer documents discussed whether the tender offer meant that the company is for sale:

Source: CMUV’s 2021 and 2023 tender offer documents

The company wasn’t in discussions or seeking indications of interest, but this language doesn’t rule out a future sale either. This situation is different at many other small community banks. So I think that management is at least open to the idea of a sale, if the price is right.

3. The order of repurchases: big tenders before open market buybacks

If you were CEO of a small bank and you had a big shareholding (say 25%), your stock was cheap and you wanted to sell the bank in a few years, what would you do? Probably repurchase a lot of shares, as cheaply as possible. That’s what CMUV did. I think the big 2021 tender offer was the first real possibility for outside shareholders to get significant liquidity for their shares. This showed in the large participation in the tender offer. There weren’t many takers in the second tender offer in 2023. The weaker hands seem to have been shaken out of the stock at that point. So now what? You think your stock is still cheap.

Perhaps now is the time for traditional on-market buybacks of your shares. This would have had a tendency to drive up the price of your illiquid stock had you done this in 2020 or 2021. It would have probably resulted in less people participating in your 2021 tender offer. So you don’t buyback shares at that point in time. You wait until there’s not much interest in the second tender offer and only then do you start repurchasing shares.

This is the company’s announcement of its first ever on-market buyback in October 2023: CMUV Bancorp Announces First Stock Repurchase Program. This is probably the ideal order to maximize the number of shares repurchased and to keep the share price as low as possible during the big tenders. Remember, this is a management team that nailed their securities positioning and debt issuance, it seems to me they would know how to optimize their tenders and on-market buybacks too.

In Q4 of 2023 the company managed to buy ~70k shares at an average price of $15.71 (look towards the bottom of the press release). So very quickly after the second tender expired in August 2023 ($14.25 purchase price) they start paying around $15.71 per share in open market repurchases, which was slightly below book value of $16.15 at that time. It looks like management still quite likes the stock at around book value.

4. A sale is the only real way for a big management payday

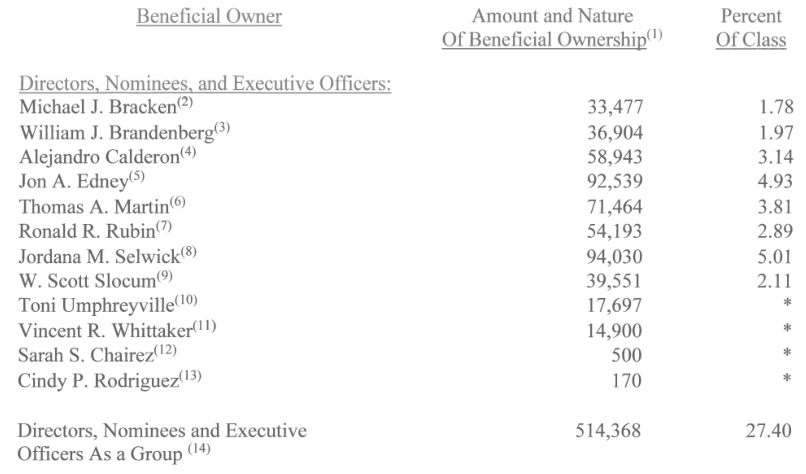

A sale makes sense for a lot of small community banks, but many don’t end up selling, or only reluctantly do so after being forced by activists in a years long process. For most management teams it makes sense to just keep raking in their salaries year after year, no matter what, because they don’t have any real stock ownership. This is different at CMUV Bancorp:

Source: CMUV’s 2023 Proxy Statement

With 27.4% ownership as of March 2023, a sale would be the only real way to get full value and real liquidity. I think the tenders and buybacks are all steps towards this ultimate goal.

5. The bank’s lack of scale and slow loan growth

Even though the bank has grown book value per share very nicely over the past few years, it should be kept in mind that the big tender offer was a huge contributor to that. With only $297m of assets, CMUV is a tiny bank. The bank has also struggled to grow its loan book. In 2020, gross loans were $207m and at the end of 2023 the gross loans only increased to $232m. That’s not impressive. Of course, if CMUV had not repurchased so many shares it could have been able to grow their loan book faster, but management apparently thought repurchases were the best option.

Regardless, growing the loan book using the bank’s retained earnings is going to be a slow process and is not the way to maximize the returns for the insiders here. That clearly is a sale, in my opinion. This management team nailed the balance sheet positioning (negligible securities), debt issuance and the tender offers. Those look like a few great capital allocation decisions to me. What could be more logical than to top it all off with a sale to a larger institution of this sub-scale bank that is struggling to grow its loan book? That would be the crown on this management team’s work of the last couple of years and this also maximizes their own returns.

6. The banks eagerness to help people tender shares

This is perhaps a bit of a strange point. I didn’t get the 2023 tender offer documents and notification at my broker until shortly before the expiry date. So I e-mailed the bank asking them whether I could participate at my broker and if it was possible to receive the tender document. I saw a lot of other cheap, small banks and I was actually considering selling. I received a very helpful answer and they said something like: we will contact the information agent ASAP to make sure everything went right and that you are able to participate.

That is not my typical experience when contacting companies. So kudos to CMUV Bancorp. This could just be an example of great customer / shareholder service, but part of me also thought: “Wow, these guys really want me to sell!”. In the end, I decided to keep my shares. After thinking about all the stuff discussed above, I thought a sale of the bank is probably in the cards within the next couple of years and I then bought some more shares.

Thoughts on merger environment and valuation

This is a bad time to sell a bank. If CMUV is open to the idea of a sale, now is probably not the time to get a decent valuation for your shares. So I don’t really expect anything to happen in the short term. The environment for bank mergers has to improve a bit. The number of bank deals is currently at very low levels. If banks recover a bit from the carnage of 2023 and interest rates stabilize for a while, things should improve again. More deals will be made and transaction multiples will increase again. I think this is just a matter of time.

Even though the environment is tough, this doesn’t mean that there aren’t investors looking for deals. One bank, also located in California, apparently secured $500m in funding to look for opportunities in the region. I’m not saying that CMUV is a potential target, but it just shows that a depressed environment also creates opportunities and that there are people waiting for the right time to take advantage of them.

As for the potential valuation of CMUV in a sale: I don’t have a great idea of what management will find acceptable. I don’t think they would consider anything below 1.3x book value. I think something like 1.5x book value would be reasonable, perhaps 1.3x if they don’t want to wait too long until sentiment improves. Mercer Capital’s Bank Watch of December 2023 has a lot of useful data about the current merger environment for banks, including valuations.

I haven’t talked about the quality of CMUV’s operations at all in this post, because I wanted to focus on the potential merger aspect here, but I think it is a reasonable bank for its size. Their ROA was around 1.4% in 2023 and prior years looked decent as well. Around 26% of their deposits were non-interest bearing at the end of 2023. I was a bit concerned that their net interest margin would get squeezed in Q4, but I was pretty happy with earnings that quarter. If the bank can make around $3.5-$4.0m (EPS around $2.00) a year for the period until a buyout, I’d be pretty happy. If earnings are much lower than that, it would be harder to justify a 1.5x book value valuation in a buyout scenario.

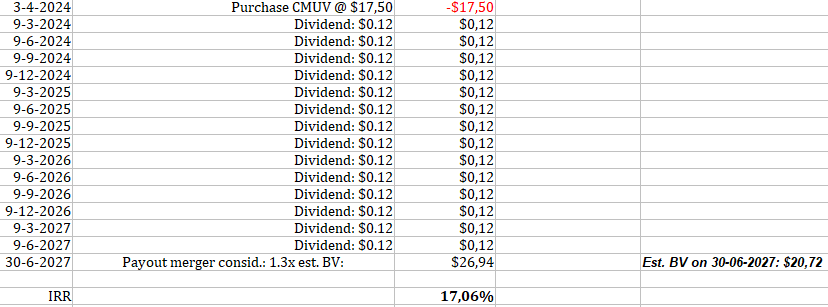

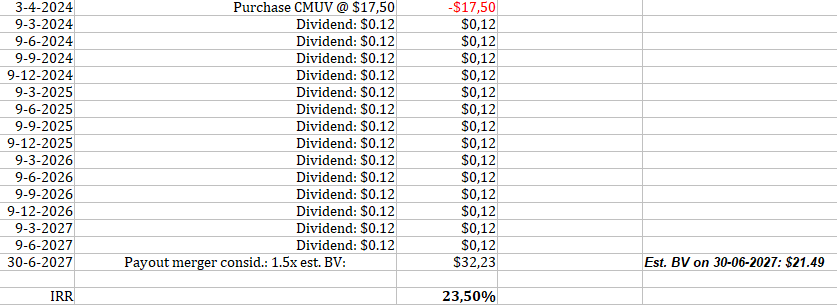

For my own entertainment I calculated two scenario’s: one where the ultimate sale price on June 30, 2027 is at 1.3x book value and EPS declines a little bit from this year’s level. And a more bullish scenario where the sales price is 1.5x book value and EPS remains stable. I could be wildly off with these numbers and it is just to give myself an idea of whether this could be an attractive situation.

Buyout scenario: 1.3x BV. Estimated BV on 30-06-2027: $20.72

Buyout scenario: 1.5x BV. Estimated BV on 30-06-2027: $21.49

I think shares are currently probably reasonably priced. I think a price around book value is probably still moderately attractive. The company has also been buying back shares around that level. Shares are currently trading slightly above book value.

I should also emphasize that I don’t think CMUV Bancorp is attractive if you don’t believe a merger is likely in the next few years. There are a lot of cheap banks to be found at the moment and it’s probably fairly easy to find something of higher quality that is trading at a similar, or lower valuation. The potential buyout is what attracted me to this situation.

Disclosure: long CMUV Bancorp (OTC:CMUV)

Disclaimer: This website is an investment journal of an individual, non-professional investor. It should be read as such.

None of the information presented on this website should be viewed as, or is intended to be, investment advice or a recommendation to buy or sell stock or any other security.

CMUV’s annual report and proxy statement for 2023 have been released: https://www.envisionreports.com/CMUV/

Most notable is probably their outlook for 2024. The financial forecast is for EPS of $2.25 and ROAA of 1.35%. I’m not sure if they are talking about earnings for the holding company (CMUV Bancorp) or for the subsidiary bank (CVB – Community Valley Bank).

They mention challenges relating to loan growth due to the interest rate environment.

The proxy shows a slight increase in the number of shares held by insiders (+7k), but thanks to share repurchases, the percentage of shares outstanding held by insiders increased to 29.2% from 27.4% last year.

I noticed the increase in “Premises and Equipment” of $2.4m. I think that probably has to do with their branch in Indigo, California. It looks like a lot of work has been done there. You can compare the foto of the branch in the latest annual report with this image from Google Streetview from August 2023: https://www.google.com/maps/@33.7088244,-116.2398788,3a,44.2y,47.91h,81.47t/data=!3m6!1e1!3m4!1sPwE9PMpZpcGFzl7hhEYBsA!2e0!7i16384!8i8192?entry=ttu