It’s been a while since I last discussed a new position. That is mostly due to the fact that I have made few changes. In the past couple of months I have mostly bought a little more of some existing positions and sold a few positions that moved up in price. Things are starting to look more interesting recently with the correction in the Chinese stock market. Some stocks in Hong Kong and Singapore have become a lot cheaper very quickly, but I have not bought anything new there yet.

One market where I have been on somewhat of a buying spree in the last few weeks is Australia. I’m finding a bunch of cheap small caps there and I’ve bought a few. One company that I bought and found very interesting is CMI Limited (ASX:CMI).

CMI Introduction

CMI Ltd (company website) is a company with a turbulent history. I will not go into too much detail in this post about all the things that have happened at this company over the last decade, but when I had read a few annual reports I was surprised about the number of events and incidents that have occurred. When you glance at the company’s results in this period you’re therefore likely to dismiss it as an investment candidate. However, today CMI is in a very different position than it was in the past. I think the important issues have been resolved and the company is now left with one high quality subsidiary.

For years CMI Ltd was something of a mini-conglomerate. The company had a financial services division that provided chattel finance to consumer and commercial borrowers, there was an engineering division and a subsidiary called TJM that manufactured and sold vehicle accessories for the 4WD and SUV markets. The finance division was sold in 2008. The engineering division was sold to an insider in 2009. In this last transaction the company provided a $17m loan to the insider who defaulted on the loan payments not much later. There were two large impairments a few years ago as it became clear that the company would not receive the repayments. This bad loan is one of the incidents that have affected the company’s financial results in the recent past.

Australian entrepreneur Ray Catelan was a major shareholder of CMI Ltd and was managing director from 2007 until 2011. He owned about 37% of the shares. Mr. Catelan passed away in 2011. Not long after, CMI was sued by an investment fund called Trojan Equity, which had a large holding in the Class A shares of the company. CMI had stopped paying dividends on the Class A shares even though is was required to do so. The management wanted to save cash to fund acquisitions. There was also controversy around a cash gift made by Mr. Catelan to his daughter Leanne that was subsequently used by her to buy a block of shares of CMI. Some discussion about this legal case can be found here. In fiscal 2012 CMI bought back the A shares for $26m.

This background story is a bit complex, but I felt it was important to add to this write-up because Leanne Catelan is today the major shareholder of the company and holds 38% of the shares outstanding. I hope this post will still be easier to understand than a Valeant 10-K.

TJM: sold

After CMI got rid of the finance and engineering divisions it still had one other problem child on its hands: TJM. This was TJM’s EBIT from 2010-2014:

Management had been trying for years to turn things around, but it never became a consistent earner for the company, losing money most years. This obscured the profitability of the company’s crown jewel: the electrical division.

I became really interested in CMI recently when I revisited the company and read that they managed to sell TJM to Aeroklas, a subsidiary of a company from Thailand called Eastern Polymer Group for $22.2 million. This was just above the book value of the TJM assets. The sale was completed on March 2, 2015. Given the performance of TJM under CMI’s ownership I think this was a great result for the shareholders.

CMI today

That means that today CMI Ltd is left with one remaining division CMI Electrical (company website). CMI Electrical specializes in the design and manufacture of flameproof plugs and couplers for underground coal mining plus specialty electrical cables, sourcing and supply of niche electrical cables, high voltage cables and flexible cables. The revenue from this division comes from the mining, industrial and construction sectors. The coal mining products have the best margins, but the revenue split between these three sectors was not mentioned in the reports.

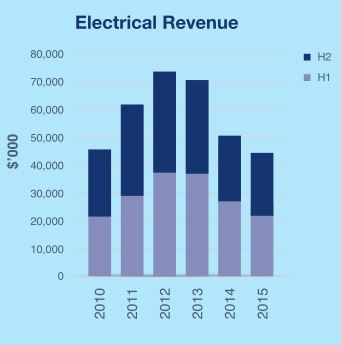

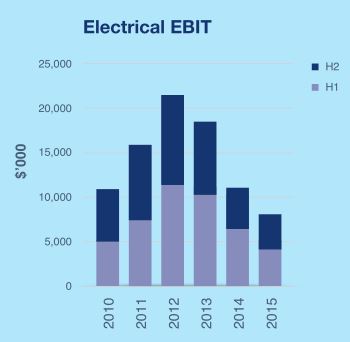

I have an old analyst report that says Minto Industrial Products has a ~70% market share. Coal prices have been falling for a while, coal mining activity has subsequently declined and the industrial and construction sectors have also slowed down. This has had an effect on CMI Electrical’s revenues and profits:

The sale of TJM has left CMI with a very large cash position. Let’s take a look at some financial data as of June 30, 2015:

Current share price: $1.65

Outstanding shares: 34,552,634

Market cap: $57.0m AUD

Book value: $60.6m

Cash: $34.2m

Total liabilities: $6.2m

Goodwill & Intangibles: $9.2m

Net income: $5.5m

Adjusted net income: $4.3m

Adjusted P/E: 13.3x

P/E excl. excess cash: 8.1x

I have made a few adjustments to the reported net income. I excluded the recovery of the impaired CMI Industrial loan ($0.87m), I’m not sure if the gain on disposal of TJM ($0.47m) is already excluded from the “Profit from continuing operations”, I think they are. My math skills are very limited in any case so I might have made a few mistakes.

The company does not look very cheap when you see an adjusted P/E of 13 and the stock selling just marginally below book value. But there are two things that are important to consider:

- At least $22.2m of the cash can be considered excess

- The current operating environment, specifically the low coal prices and decreased mining activity

Excess cash

After the sale of TJM the company mentioned that it was looking for suitable acquisitions that were complementary to the CMI Electrical division. In the latest annual report the current chairman Mr. Buckley mentioned that the company has not succeeded yet in finding an acquisition candidate and that CMI is now considering returning the proceeds of the TJM sale to shareholders:

“The Board notes that suitable acquisitions with synergies with the existing business have as yet not been identified and as a result the Board is considering the potential of a capital return of up to $22.2m (the proceeds from the TJM sale). The Board is seeking a tax ruling in this regard.”

So I think at least $22.2m of the current cash balance of $34.2m can be considered excess. When we exclude this amount from the current market cap it means we are paying just $34.8m for the remaining business that generated adjusted net income of $4.3m in fiscal 2015: an adjusted P/E of only 8.1x.

What is a normal operating environment?

I’m not a coal mining expert and know little about economic cycles in general. I do know that the current operating environment in Australia and other countries that rely on mining and natural resources is very depressed. At some point things will probably pick up a little, even though it will probably not be anywhere near the levels seen when the Chinese economy was booming. CMI Electrical’s EBIT was north of $20m in 2012, in 2015 it was $8.1m. It is impossible for me to say whether the bottom has been reached.

Business does appear to have stabilized somewhat. Another quote from Mr. Buckley in the latest annual report:

“Lack of capital investment in new coal projects has continued to impact sales from the division’s mining product range. This has been compounded by a lack of new infrastructure projects which has kept revenue from the building and construction product range down. Overall revenues are 12% down but activity levels have been consistent with the second half of 2014FY indicating that sales activity has not decreased further in the course of 2015FY.

Noting that revenue has stabilised, the Board’s view is that the outlook for the business in the medium term remains positive, with an expected improvement in the market over the next couple of years. Revenue from new initiatives including Flameproof and some new product distribution opportunities will begin to flow during the 2016FY. The Board continues to look for more synergistic acquisitions and organic opportunities to grow this division.”

Conclusion

I think CMI is a nice vehicle for investing in a mining recovery. The upside is much less dramatic than investing in some of the companies directly involved in the field, but your downside protection is much stronger with CMI. CMI has more than half its market cap in cash, no debt and a business that is pretty lean in terms of working capital requirements and capital expenditures.

I don’t know what the operating environment for CMI Electrical will look like a few years from now, but I do think it is likely to be better than today. Meanwhile CMI will pay a nice dividend if it can: the company has just declared a $0.06 dividend with a record date of September 4, 2015 and a payable date of September 18. The fact that the company is willing to return cash is positive on two levels. It gives an indication that minority shareholders will be treated fairly, something I was a bit doubtful about after reading about the lawsuit by Trojan Equity and the purchase of a block of shares by Leanne Catelan. It is also something of a vote of confidence by the management about the near term future of the business: if they were worried about revenues dropping strongly from here and the company losing money, they would probably hold on to all the cash. Instead they are considering returning a substantial part of it.

I have not discussed the historical results of CMI Electrical in this post much. The older annual reports do show segmental information of TJM and CMI Electrical in the footnotes. It shows quite clearly that CMI Electrical was by far the better business and that their capital expenditures have been quite low: in 2014 and 2013 just $800k and $443k respectively (page 67 of the 2014 AR). I do think you should add some capitalized product development expense to this amount, but I think that total capex will not be more than $1m – $1.5m per year on average. The electrical business looks to be very cash generative. In a business environment that is less depressed and without the anchor of TJM dragging down the results the quality of CMI’s current business should become clearer in future reports.

Edit Sept. 3: Just found a few old write-ups of CMI Ltd on VIC that provide much more detail about their mining products:

- Dec. 2008: http://valueinvestorsclub.com/idea/CMI_Limited/3531

- Mar. 2013: http://valueinvestorsclub.com/idea/CMI_Ltd/92085

Disclosure: long CMI Ltd (ASX:CMI)

Interesting. Why would the purchase of a block of share be a red flag? Was the gift made from company cash?

And was the current board in place when it happened?

No, it was a cash gift from Mr. Catelan. I think the conflict with Trojan Equity might have already been unfolding at that time, I’m not sure.

The problem is that there are rules for how much stock one can buy in a single transaction when you’re deemed an “associate”. From the article I linked:

“But the panel reasoned the stockmarket purchase notice did not declare an association with Mr Catelan. So the panel investigated with an emphasis on regulations about how much stock people deemed associates can buy in one swoop, once they own over 20 per cent.”

It looks to me that the gift might have been made to increase control over the company so potential activists would have a much harder time gaining control. That is not a sign of shareholder friendliness.

There have been some board changes since then I believe. But in a case like this with a major shareholder owning 38% I think you cannot expect too much from other board members anyway. It’s the behavior of the major shareholder that dictates things.

I don’t think the buy of the block of shares was a wise move. In my view it doesn’t meet Buffett’s “front page test”. When you search Google for “Ray Catelan” the quoted article is the second result. I wouldn’t like that.

I’m not too concerned about this transaction btw. I think the company has steadily moved in the right direction and believe minority shareholders will be treated fairly.

It’s a non-issue, imo. Aus has prob the worst corp gov in the world, so going in you would know what to expect. Same as the fund who held (still holds?) the preferreds. They should have read the prospectus and assume the worst. Prefs are a crappy choice in most cases anyway.

Most important is whther the underlying biz is worth it, imo.

Nice idea and beautiful writeup! Thank you for that and I am long.

Insider buying supports the bull case: Andrew Buckley, executive chairman, has been buying 40.000 shares at 1.51 and 85.000 shares at 1.56 in March and February this year respectively. He bought the shares with money out of his own pocket, not stock options.

Thanks!

Yes, it’s good to see a few insider buys. Mr. Buckley also has 900,000 share performance rights, of which 300k are already vested and another 600k max. will become vested if the company achieves 15% EPS growth per annum over the entire measurement period that started on June 30, 2014 (EPS: 10.29 cents).

So I think the incentives are in place. I don’t think the EPS targets are ambitious enough though since the 2014 earnings were so depressed. You should not be rewarded for operations normalizing simply due to the general ebbs and flows of the economy.

Mr. Buckley reported a sale of ~30k shares today. I’m not too concerned about relatively small insider sells, but of course it would be better to see insiders buying or holding. It might be a sell for diversification purposes, since 300k of the performance rights have now vested and his common holdings went from 227k to 527k.

I am not too concerned. But it is a weird manoeuvre: effectively Mr. Buckley bought the 30k shares for 1.51 in March and then sells them for 1.64 six months later. Including dividend, he made 0.19 profit per share for a total profit of 5.700 AUD. I wonder if this is enough to cover the administration / accounting expenses.

Mining is very likely to go into a protracted downcycle after booming/supercycle for the past two decades. China’s economy is very likely to stagnate if not collapse pretty soon.

Besides, don’t see any significant margin of safety at the current price point.

I think those expectations about mining/China are more than reflected in the current market price.

I do see a margin of safety, considering the large cash balance and the currently profitable operations during a bust in the mining cycle. What should also help the company is that their coal mining products are necessary for the safe operation of a mine and need to be replaced over time (the VIC write-ups provide more detail). So even during a prolonged bust I think there will be a base level of revenue for replacement products. We’ll see.

Hi there,

Great write-up! I’m also interested in buying shares in this company. Right now I’m looking into the dividend and withholding taxes. I read they are paying a ‘fully franked’ dividend and that there is no withholding tax on fully franked dividends. I myself am a Dutch resident. Some time ago they paid out a AUD 0.03 dividend. Did you have to pay any tax on the pay-out?

Hi Joris,

There was no withholding tax charged by my broker (IB).

By the way, not much interest in this stock from outside Australia:

“26. As of 16 September 2015, CMI had 34,852,634 ordinary shares on issue. 85,676 of those ordinary shares were held by non-residents.”

Source: http://law.ato.gov.au/atolaw/view.htm?docid=%22CLR%2FCR20164%2FNAT%2FATO%2F00001%22

I think those ~86k shares are just those held by non-residents personally, under their own name. If you hold them through a broker based in the US or Europe and they use an Australian subsidiary or bank to hold those shares, then that subsidiary / bank would be seen as the holder of the shares and a resident. You would be the beneficial owner of the shares though. So, I don’t think that number is the “look-through” number of shares held by non-residents.

The annual report for 2016 just came out. Revenue and profit decreased, but not alarmingly so. I get for PE (adjusted for excess cash) 2.5 and EV/EBITDA of 1.6. This seems spectacularly cheap for a not very bad business. I wonder when the price is going to jump.

I agree, it looks very cheap.

Given the very tough conditions for the coal mining industry, I think CMI’s results look reasonable.

I still agree with my thoughts from the write-up from last year. I think CMI offers strong downside protection from their large cash balance and a resilient business. Even in a very bad operating environment they are still reasonably profitable and cash generative. The total amount for Property, Plant & Equipment on the balance sheet is just $0.5m. Payments for plant and equipment were just $27k and expenses for intangible assets were $276k, which just confirms that the business requires little capex.

If coal mining picks up a little, results should improve and there should be substantial upside from this price, in my opinion. Most investors don’t want to touch anything even remotely connected to coal mining, so I think that is what is holding down CMI as well.

I don’t mind holding on and waiting. Even after the 10% jump of the share price after the results came out, CMI is still trading at just 0.94x NCAV. There are very few profitable, cash-rich, cash generating, dividend paying net-nets out there in the world today, especially outside of Japan.

Surprising development: CMI changes their business into an investment business. I would have preferred for them to just buy back shares with their 20M in cash. But I guess there is not much we can do about this.

I read their prospectus where they are offering to buy back 10% of the shares. The manager’s benchmark for the investment business will be RBA Cash rate plus 2%, i.e. 3,5%. That is a laughably low hurdle to jump for investing in such a risky asset as small cap.

I think they deliberately make the buy back offer look attractive (i.e. their company unattractive). I am keeping my shares.

Yes, I don’t like this proposal at all. A reason some of these cash-rich companies trade at a big discount to intrinsic value is that investors fear that management does something dumb with the money. I think that the CMI management might be doing that here.

I might write a post about this with some more detail, but I don’t like the manager they have chosen (Glennon Capital). Michael Glennon seems like a speculative growth investor who has had a few good years. He also comes across as a promoter / salesman. I don’t like the biggest holdings in their Small Companies Fund. As you point out, the hurdle is ridiculous as well.

If Glennon can identify bargains, and the directors themselves indicate in their latest shareholder letter that CMI is cheap, why doesn’t he own a single share of CMI? Why do they want to appoint a non-owner as a director and a manager of their excess cash?

I’m not sure what I’m going to do. I don’t think foreigners can participate in the buyback anyway. I don’t like the prospect of Glennon managing CMI’s excess cash though. It’s not just the $20m that they have committed. Future excess cash is probably also going to be invested by Glennon, so this part of the business really becomes a very important part of the overall valuation. I have just not seen anything yet that gives me confidence that Glennon Capital is a good, value oriented investor capable of outperforming an index like the ASX.

The idea of taking a portfolio approach to the company isn’t necessarily bad, but picking the right manager is essential. I just have a lot of doubts about Glennon Capital. These are just my first impressions. If anyone has come across some long term data that shows Glennon can outperform, I would like to see it.

I am an Australian (living in the US) and am relatively familiar with this business.

I agree with the comments regarding Glennon but with the backdrop of this company now trading at an EV/EBIT of 1.2x (off the lowest earnings of the last 10 years) I would make the following comments:

– Even in the hands of a bad stock picker which Glennon may be, it is hard to see that he would turn the $20m into less money over time with a diversified strategy

– As ludicrously low as the performance hurdle is at least there is some alignment of incentives as he still needs to generate positive returns reasonably above the cash rate to make money (the 1% management fee on a $20m base is obviously fairly negligible)

– If I have read the prospectus correctly, half of these management fees are actually payable to CMI itself so shareholders are effectively paying themselves half of these fees mitigating the negative impact of what is a generous arrangement

– There was an earlier comment about Australian corporate governance being poor. As someone who has invested on exchanges (and in private companies) around the world that is laughable. Australia has some of the best protections for shareholders worldwide. I would feel safer with my money in an ASX company than on almost any other exchange in the world. The kind of nonsense companies get away with on the AIM or on German lower exchanges would not be tolerated

To put this in perspective, if Glennon somehow managed to destroy $10m of value in this portfolio the operating business would still only be trading at 3.4x EBIT off a cyclically low earnings number. The bigger issue I have with the company is the lack of disclosure around its core business’ operations, strengths, threats and risks. Having said that it has been consistently profitable for a long time and there doesn’t appear to be any reason to believe it is in a terminal decline even if coal investment activity never returns to the 2008-2013 levels.

I’m not surprised TJM performed poorly. When the majority of their manufacturing went offshore to China the previous good quality dropped considerably and loyal consumers reacted accordingly. I am in the auto aftermarket industry and was disappointed to see another good Aussie name producing sub par goods. Hopefully Aeroklas have raised the bar since their purchase.

Some good news in het latest report: they have been buying back shares: 10% of total. With market capitalization less than equity, I hope they keep on buying back and I will keep the last share :-).

Hi Farbelow,

I think that was the 10% buyback that was done as part of the change of business to an investment company. I don’t think they’ve been doing repurchases in the open market. I’ve put some of my thoughts together about CMI in a new post: https://www.valueinvestingblog.net/cmi-update/

Yes, you are right, I was to quick to cheer.